Surety bonds are a form of protection that dates back to Babylonian times. Such bonds are a key piece of many public and private sector transactions. U.S. Customs, for example, requires importers to carry bonds to ensure compliance with rules and regulations. Courts require bail bonds to release criminal case defendants. Property or project owners require contractors to carry performance bonds.

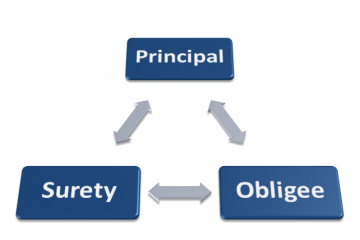

In the U.S., surety ship is considered a form of insurance and is regulated accordingly. This is something of a misnomer since insurance is typically a two party transaction, while surety bonds are a three party transaction. The three parties to a surety contract are:

Principal: The party that takes out the bond as a guarantee against a stated obligation.

Principal: The party that takes out the bond as a guarantee against a stated obligation.

Obligee: The party to whom the guarantee is made by the surety on behalf of the principal. In the above examples, a property owner, U.S. Customs, and the Airline Reporting Corporation are potential obligees.

Surety: The entity that steps in and pays the obligee in the event of a specific failure to perform or meet an obligation on the part of the principal.

There are two primary categories of surety bonds. Contract Surety Bonds and Commercial Surety Bonds. Contract Surety Bonds provide financial security and construction assurance on building and construction projects by assuring the project owner (obligee) that the contractor (principal) will perform the work and pay subcontractors, laborers, and material suppliers.

Contract surety bonds include:

- Bid bonds – financial assurance that the bid has been submitted in good faith.

- Performance bonds – protection for the owner from financial loss should the contractor fail to perform the contract in accord with its terms and conditions.

- Payment bonds – guarantee that the contractor will pay certain subcontractors, laborers, and material suppliers associated with the project.

- Maintenance bonds – guarantee against defective workmanship or materials for a specified period.

- Subdivision bonds – guarantee to a city, county, or state that the principal will finance and construct certain property and infrastructure improvements.

Commercial Surety Bonds guarantee performance by the principal of the obligation or undertaking described in the bond.

Commercial surety includes:

- License and permit bonds – required by state law or local regulations to get a license or permit to engage in a particular business.

- Judicial and probate bonds, also known as fiduciary bonds – secure the performance on fiduciaries’ duties and compliance with court order.

- Public official bonds – guarantee the performance of duty by a public official.

- Federal (non-contract) bonds – those required by the federal government, e.g. Medicare and Medicaid providers, customs, immigrants, excise, and alcoholic beverage.

- Miscellaneous bonds, e.g. to guarantee employer contributions for Union benefits, and workers’ compensation for self-insurers.

One of the main differences between an insurance and surety contract is that an insurance premium is usually based on a certain expectation of losses. Surety contracts are designed to prevent loss, according to the Surety Information Organization (www.sio.org). In this model the underwriting process involves pre-qualification and the bond is underwritten with little expectation of loss. The premium is mainly a fee for pre-qualification services. In some cases a surety company will require indemnity of the owners of a closely held corporation. The two main reasons for this requirement are that the surety company requires all personal/business assets to back the guarantee and that there is less chance a principal will avoid stated responsibilities if personal/business assets are at stake. If an underwriter is unable to approve a bond request based on the qualifications given by the principal, the company may suggest depositing some form of collateral as an inducement to write the bond. In practice, many bonds are written on this basis, particularly ones that are considered financial guarantees.

The Andrew Agency

Obtaining a surety bond is like opening a line of credit. And similar to a banking experience, developing a long-term relationship with a surety company can be an important step for you or your business. Call The Andrew Agency at 804.320.2886 for further details on surety bonds and how they apply to your business.